2023.11.26 Hyundai Motor Company

Hydrogen Inside 2

Hydrogen gas, with its low energy density per volume, is highly inefficient to transport in its gaseous form. Therefore, it's essential to physically or chemically alter and store hydrogen before transportation to improve energy transport efficiency.

Physical conversion involves compressing or cooling hydrogen gas to extreme cryogenic temperatures to create liquid hydrogen. Chemical conversion utilizes chemical reactions to transform hydrogen into other substances like ammonia. Let’s explore the details of these methods for hydrogen storage and transportation.

Currently, the most common way to transport hydrogen is to compress it to a high pressure and then transport it by tube trailer. This method is relatively simple because it does not require any other conversion process other than gas compression.

However, the amount of hydrogen that can be transported using tube trailers is limited, and it is expected to be far insufficient compared to the demand in the future hydrogen society. That's why further research is necessary to develop more efficient and cost-effective methods for hydrogen storage and transportation.

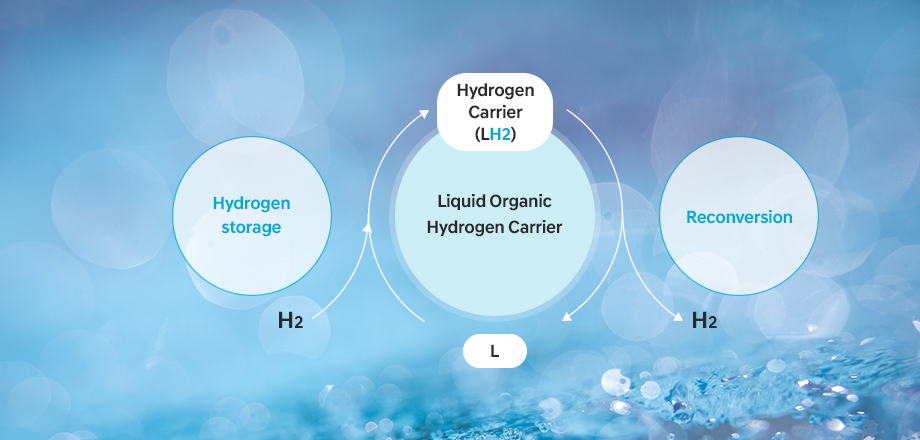

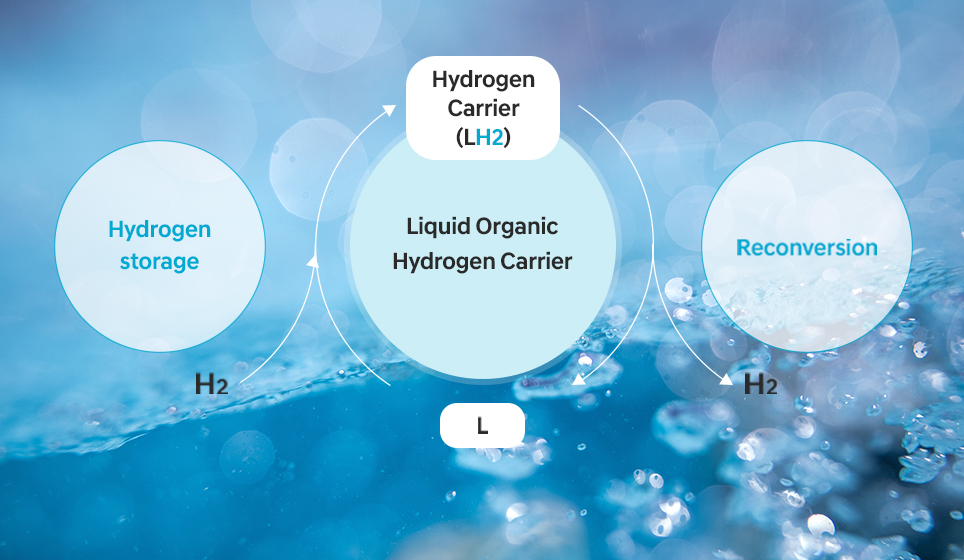

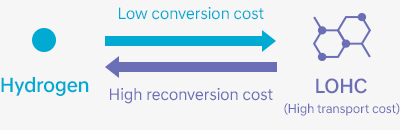

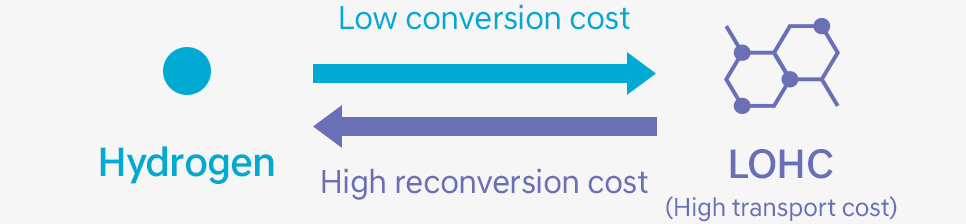

LOHC, also known as Liquid Organic Hydrogen Carrier, is a liquid compound obtained by adding other substances to hydrogen. It remains in a liquid state under ambient temperature and has a higher hydrogen storage capacity. A key benefit is its compatibility with the existing oil transportation infrastructure.

However, there is a drawback in the reconversion process of extracting hydrogen from LOHC for utilization, as it requires significant energy and incurs additional costs. Overcoming this challenge will be a determining factor for the commercialization of LOHC.

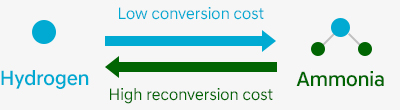

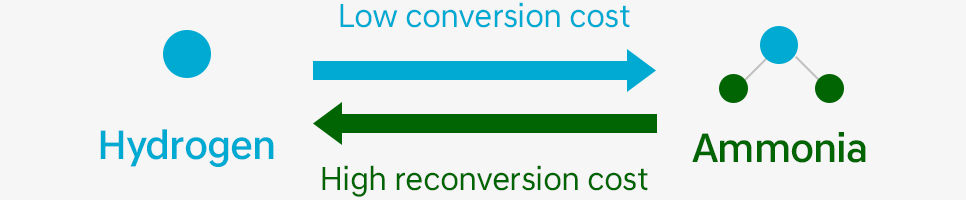

Ammonia (NH3) is a chemical compound of three hydrogen atoms and one nitrogen atom. This means that we can produce ammonia from hydrogen or extract hydrogen from ammonia, enabling convenient storage and transportation of hydrogen by converting it into ammonia.

Ammonia has a high hydrogen storage density per unit volume and already has an established value chain in the storage and transportation sectors as it is widely used as a fertilizer. Therefore, the commercialization of storage and transportation is expected to be easily achievable.

However, there are challenges that need to be addressed. Converting hydrogen into ammonia and then reconverting ammonia back into pure hydrogen involve multiple processes with significant costs. Moreover, the commercialization of the cracking process to revert ammonia into pure hydrogen has not been realized yet.

When hydrogen is cooled to below -253℃, it changes into a liquid form, reducing its volume significantly. This process makes liquid hydrogen storage highly efficient, as it occupies 1/800 of the volume compared to its gaseous form. This allows for efficient large-scale storage and transport. Moreover, the reconversion process is relatively straightforward, as liquid hydrogen vaporizes when the temperature rises.

In other words, keeping hydrogen in its liquid state means maintaining it at a cryogenic temperature below -253℃. Until now, this has required a significant amount of energy and cost. Furthermore, a phenomenon called boil-off gas (BOG) occurs and results in the loss of liquid hydrogen through natural evaporation, making long-term storage difficult.

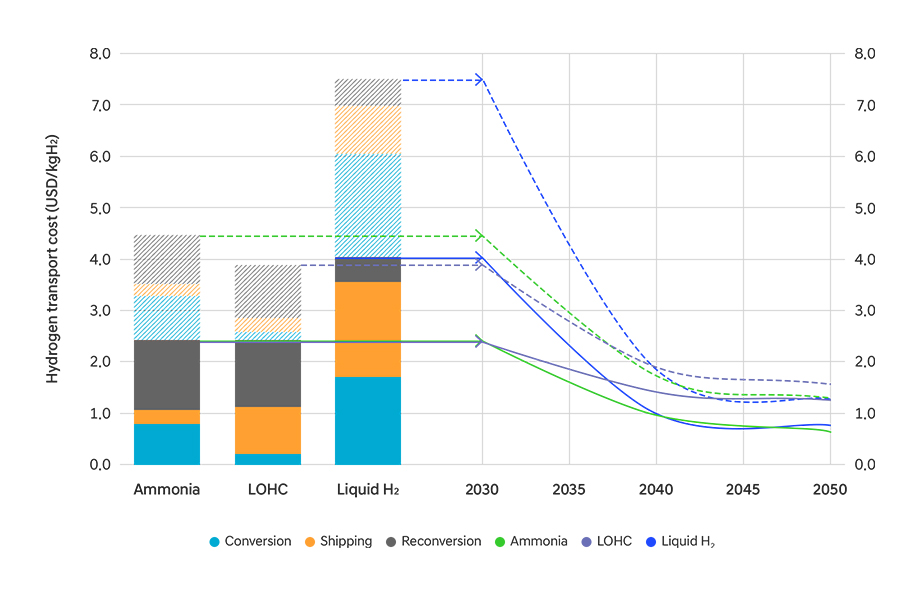

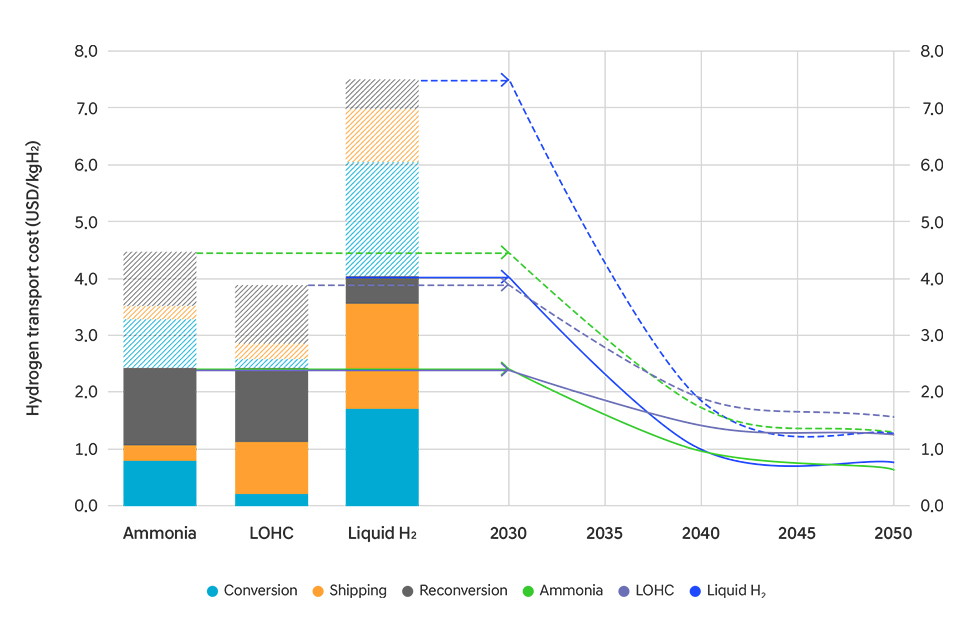

Figure 1 shows the anticipated transport cost for ammonia, LOHC, and liquid hydrogen from 2030 to 2050. Optimistic estimates are represented by the solid areas and solid lines, while the shaded areas and dashed lines represent a pessimistic scenario. Also, the colors in the areas indicate the proportion of costs for conversion, shipping, and reconversion.

First, let's consider the trends in transport costs. By 2050, the transport costs for ammonia, LOHC, and liquid hydrogen are all expected to decline. Notably, by 2030, ammonia and LOHC's transport costs seem relatively more cost-effective than liquid hydrogen. Over time, the economic efficiency of liquid hydrogen is predicted to improve and reach a level similar to that of ammonia and LOHC by 2050.

What's the reason behind this? Let's take a closer look. For green ammonia, the process of converting hydrogen into ammonia is already commercialized and the cost is relatively low. However, the high cracking (reconversion) cost serves as a factor that contributes to the overall cost increase. This suggests that research on the cracking process, which can lead to potential cost savings, is necessary for ammonia production.

Similar to green ammonia, LOHC also has a significant proportion of reconversion cost when refining LOHC back into hydrogen. However, LOHC has lower conversion costs and higher shipping costs than green ammonia.

For liquid hydrogen, on the other hand, the costs for hydrogen liquefaction and shipping are extremely high. However, the process of reconverting liquid hydrogen back into gas through simple vaporization doesn't significantly impact the overall cost. Therefore, research on developing technologies for the production and shipping of cryogenic liquid hydrogen and improvements in storage tanks could be key to reducing these costs.

As mentioned in 'Hydrogen Inside 1', imbalances in green hydrogen production costs among countries are expected in the future. Therefore, developing cost-competitive hydrogen carriers is necessary, and such development will serve as a stimulus to the global hydrogen trade.

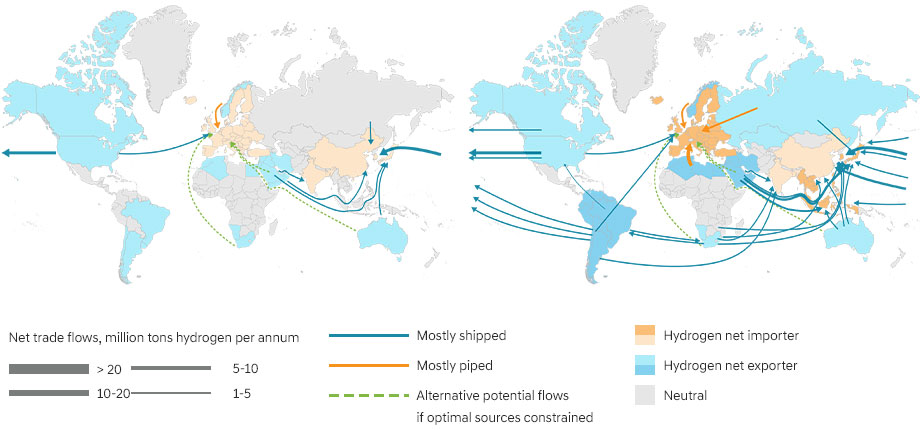

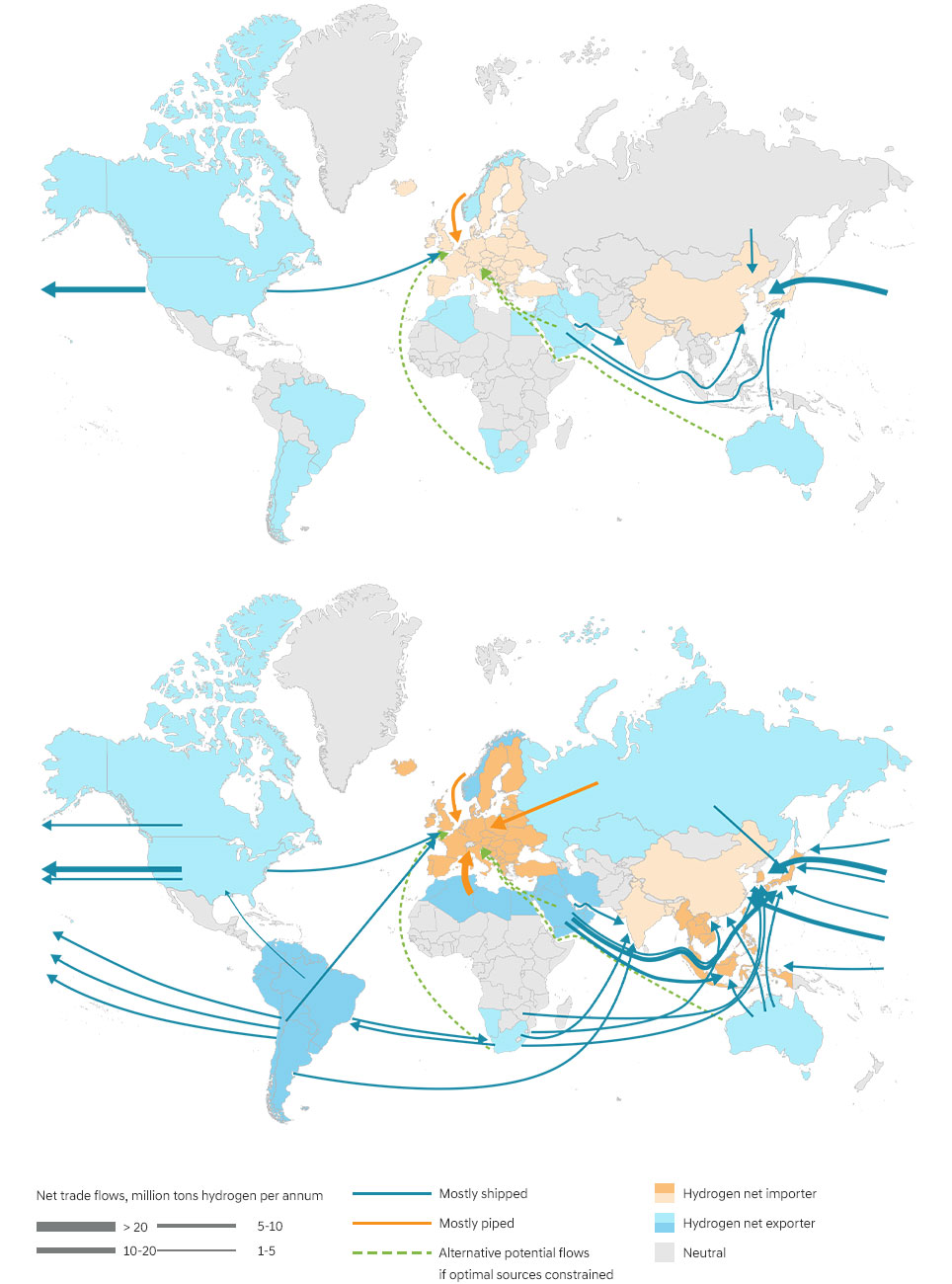

Figure 2 shows the global hydrogen trade outlook for 2030 and 2050. The orange regions represent countries that import hydrogen due to their hydrogen consumption outpacing production, while the blue regions represent the countries that export hydrogen. The gray regions represent where hydrogen demand and supply are expected to either reach a balance or be non-existent.

By 2030, early trade routes are expected to be established. Around 10 trade routes will comprise volumes of more than 1 million tons per annum (MTPA), while a variety of other smaller trade routes will begin to emerge. Japan and South Korea, where hydrogen production costs are relatively high, are expected to rely primarily on maritime shipping for their hydrogen imports.

By 2050, it's likely that there will be more than 40 different trade routes each with a capacity of over 1 MTPA, with the largest reaching up to 20 MTPA.

Just as we currently trade energy through fossil fuels, hydrogen is expected to take up a significant portion of future energy trade. With hydrogen emerging as a new energy source, countries and companies worldwide are actively entering hydrogen-based industries to take the lead.